Roaring Crisis

Among the many ripple effects of the 2008/09 Global Financial Crisis, two interrelated outcomes stand out as perhaps the most unexpected. First, the so-called “Marx revival” was made possible by the deep global crisis, which strongly corroborated his argument that capitalism is inherently unstable. Mainstream economists, who adore steady states and equilibria, lack any substantive theory of crisis, while some others, bolder still, championed the idea of endless growth. The deep recession blindsided them, and they were unable to provide any rational explanation for such a momentous event—never mind their sophisticated mathematical models.

Marx, by contrast, did have one. Overproduction, unemployment, relentless recessions, rising inequality, and ensuing social unrest—all were firmly part of his critical arsenal. Instantly, his unexpected rebirth was met with a red carpet welcome, even from mainstream publications like The Economist. It’s worth stressing that this revival was not based on Derrida’s Specters of Marx or the tedious, dogmatic orthodoxies of Soviet “Marxists” and their accomplices. Instead, it went back to the primary sources—no interpreters needed.

Second, the emergence—albeit with a slight delay—of revitalized social movements. Public outrage over the massive public bailout of reckless private financial institutions, all without a shred of accountability, finally reached a boiling point in 2011. While “too big to fail” became the defensive mantra for those responsible and their government backers, the crowds—directly and indirectly affected—were far from ready to move on.

Occupy Wall Street took the lead with its memorable “We are the 99%” rallying cry, which quickly echoed around the globe, resonating especially in the Middle East through the Arab Spring. Even if these movements’ long-term structural impact proved minor, the predicted social unrest was more than just a threat. Inequality became its core political target. The new movements also openly questioned the dubious government policy of propping up losers with billions—a policy I have previously labeled as social(rich)ist.

While the true nature of these social movements remains up for debate, it was social media and digital technologies that crowded out the headlines—often at the expense of the movements’ genuine socioeconomic and political aims. At some point, we were told, almost breathlessly, that social media and mobile apps sparked the upheavals—without them, apparently, nothing much would have happened. These technologies were celebrated as radically revolutionary, the handiwork of Silicon Valley’s most inventive minds.

Today, though, it’s just as easy to argue the opposite: these technologies are, if anything, counter-revolutionary. The aura has faded; their true colors, some would say, are finally showing. Personally, I don’t see digital technologies as simple tools—like a hammer you grab and use. They are mostly privately owned social endeavors. And their proprietors call the shots, guided by superprofits, political context, and personal preferences. Don’t just take my word for it—look around you.

Inequality, Rising and Vanishing

By the end of 2011, income and wealth inequality had fully infiltrated the public sphere—though not always in line with Habermas’ hyperrational communicative action theory. The conversation was heated and urgent, yet genuine policy proposals and concrete steps to tackle the challenge were noticeably absent. Against this backdrop, Piketty’s now-famous book on capital and inequality landed: first in French in August 2013, then in English eight months later. It unexpectedly sold over 2 million copies—a remarkable feat for a dense and thick academic tome filled with accurate charts that, I must admit, did not win me over aesthetically. Piketty also offered a few policy recommendations promptly dismissed by mainstream media and economists as unrealistic, of course!

A couple of months before Piketty’s French edition hit the shelves, The Guardian was already making waves with the first Snowden NSA revelations. Suddenly, surveillance shot to the top of the public agenda, jostling with inequality for top billing. Unchecked surveillance did provoke resistance—people mobilized to challenge these shady, unlawful practices—but it failed to ignite any new social movements.

From where I sit, surveillance and inequality are not rivals; they’re two sides of the same coin, at least when it comes to human rights. Surveillance lands squarely in the civil and political rights camp, a domain that has shaped political discourse since the 1980s. Inequality, by contrast, is tucked into the economic, social and cultural rights realm—a set of rights still awaiting ratification in a surprising number of countries, not least the global hegemon. All of which suggests that, in the world of policy, surveillance issues get the lion’s share of attention and action, leaving inequality to endlessly wait its turn—pretty much like Beckett’s Waiting for Godot.

The public sphere’s fixation on inequality and surveillance peaked in 2015. Soon after, the tide began to turn with the rise of fake news and the so-called post-truth society, followed by the COVID-19 pandemic, which unleashed yet another global economic crisis. Today, a few still push these envelopes. But the pair now look more like two bulky old trees standing in a forest where taller, stronger siblings overshadow them. We know they are there, but we have grown accustomed to seeing them every day to the point that they have become almost invisible.

Nevertheless, that does not mean they have vanished in practice, nor that they have become less relevant socially. In the case of conspicuous inequality, old and newly minted billionaires with unprecedented global power, who frequently tell us how the future will look, provide a perpetual, stark reminder.

In this context, it is thereby unsurprising that the 2026 World Inequality Database (WID) report attracted little attention. As expected, the document shows that global inequality is increasing. While the bottom 50% of the world’s population have a share of 8% of total income or 2% of total wealth, the top 10% have 53% and 75%, respectively. The situation across regions is also dismal. The average monthly income in sub-Saharan Africa is only 7.9% of that in North America and Oceania. Latin America and the Caribbean do a bit better with 28%, but South and East Asia cannot cross the 16% line. At the same time, many of these countries face sharp inequality. That sounds like a double whammy that undoubtedly poses increased policy and developmental challenges.

Inequality and Economic Growth

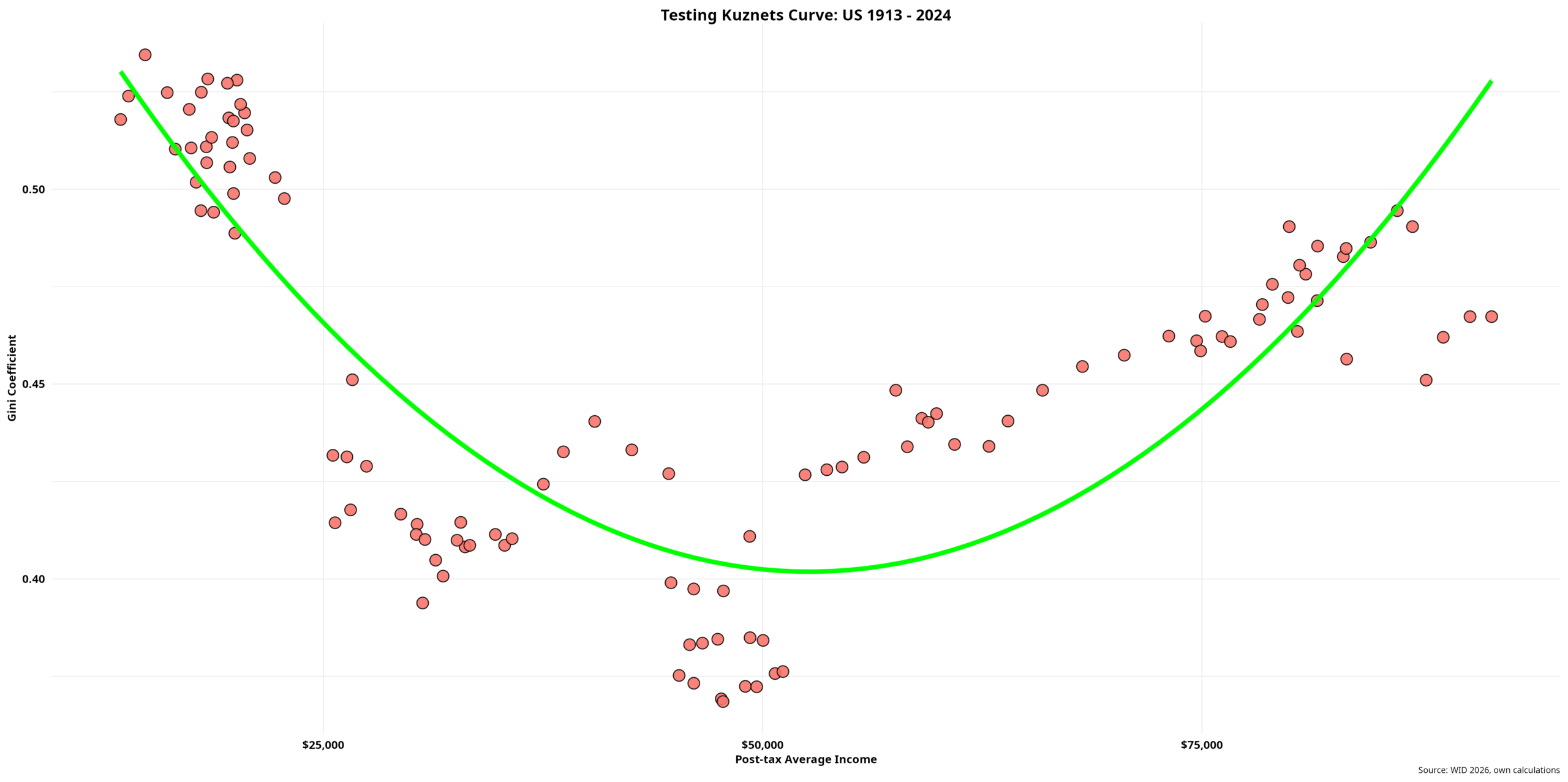

The connection between income and inequality has been revisited time and again. It traces back to the famous Kuznets’ inverted-U hypothesis: inequality rises in the early phases of development, only to recede as income crosses a certain threshold. Pinning down exactly where that threshold lies is notoriously tricky, since it depends on specific structural shifts in the economy. But before wading deeper into the theory, let’s take a brief look at the U.S.—the classic case study, thanks to its wealth of historical data, especially using the latest WID numbers.

The graph below shows post-tax average national income in 2024 dollars and the Gini coefficient (click to enlarge). The bright-green line is the basic regression line that illustrates Kuznets’ hypothesis: the Gini coefficient as the dependent variable regressed against the log of average income and the log of average income squared (G = log(ni) + [log(ni)]^2 + et).

This result is precisely the opposite of what we expected, as we obtain a U-shaped curve that is not at all inverted. Such a result is, in fact, one of Piketty’s main findings in his massive 2013 book. So we should not be that surprised.

However, that is not the end of the story, as we will see in the next post.

Raul