Back to Kuznets

A cursory overview of Kuznets’ personal and academic background reveals his distinct approach to economics, in contrast with the marginalist school. Having migrated to the U.S. in 1922, he then completed his Ph.D. in economics at Columbia University four years later under the supervision of W. C. Mitchell. Mitchell, one of the co-founders of the New School for Social Research (NSSR) in 1919, my alma mater, also founded the National Bureau for Economic Research (NBER). He spent most of his professional career studying business cycles and was considered an institutionalist. He was certainly not a fan of general equilibrium theory, yet he made important contributions to quantitative economics.

Kuznets followed his advisor closely and eventually surpassed him. His mother tongue allowed him to read Kondratiev’s work on long waves almost 50 years before it was fully translated into English. In that light, Kuznets curves, used by the Speculative Kuznets Team (SKT) to support his hypothesis, drew on long-wave theory and constituted his response to the Russian author and, indirectly, to Mitchell and Schumpeter. While his early postdoctoral work focused on production and prices, he later turned his attention to national income accounts and the measurement of economic growth (GDP). The latter work opened the door to the 1971 “Nobel Prize” in economics.

Kuznets and Mitchell can be considered empiricists with the caveat that they did not discard theory completely. On the contrary, they relied heavily on inductive reasoning—starting with hard data to identify emerging challenges or newly discovered patterns. Once these patterns were properly delimited, they advanced theoretical arguments to offer coherent explanations while calling for additional data to corroborate key hypotheses. This whole process could then repeat itself, following a successive approximations approach. Both were also open to injecting historical and institutional elements into the explanatory formulation, thereby moving beyond mainstream economic frameworks. In my view, Kuznets would thrive in today’s era of big data and AI, as data and computational capacity always seemed to trail behind his groundbreaking ideas. In any event, the now world-renowned March 1955 article follows that same epistemological strategy.

Paper Overview

I first read the paper in the early 1980s when I was studying economics at NSSR. It did not make an impression on me at all. We knew that inequality in industrialized countries was already increasing, while it never really declined in developing economies. Other than the main hypothesis, I could not recall any of its contents. Subsequently, I encountered the environmental Kuznets curve in the mid-1990s. However, that did not change my mind. Many advanced countries’ economies were shifting toward financial services while simultaneously outsourcing manufacturing and thereby carbon emissions to the developing world. Piketty’s bestseller just reinforced my views.

Re-reading the paper recently was a much-needed refresher and a bit of an eye-opener.

The paper comprises five sections, preceded by a rather long introduction. There, Kuznets posits the key question: Does long-term national income inequality increase or decrease with a country’s economic growth? He immediately goes into a detailed discussion about the lack of adequate data to fully test his research question, painstakingly pinpointing the difficulties involved in compiling and creating it. He concludes by saying, “…I have difficulty visualizing how such information could practically be collected…” (pg. 2). Maybe that is part of the reason Kuznets moved on to other subjects soon thereafter. On the other hand, one could argue that the work of Piketty, among others, made such visualization possible.

The first section examines trends in income inequality in advanced capitalist countries. The next two sections explore theoretical explanations for such trends, offering a wide range of structural and institutional factors that could support his hypothesis. Section IV compares developed and “underdeveloped” countries, where he finds striking differences. The last section is his summary of findings and research recommendations.

The concluding remarks are indeed remarkable yet frequently ignored by both supporters and critics. As a good empiricist, the author is keenly aware of the “meagerness” of relevant data on income and inequality. He then adds, in a moment of stunning intellectual honesty:

“The paper is perhaps 5 per cent empirical information and 95 per cent speculation, some of it possibly tainted by wishful thinking. The excuse for building an elaborate structure on such a shaky foundation is a deep interest in the subject… The formal and no less genuine excuse is that the subject is central to much of economic analysis and thinking…” (pg. 26).

Speculation here is not the same as the Hegelian speculative reason I used to classify the various Kuznets teams. In any case, given the topic’s fundamental nature, the direction of future research is crucial for Kuznets. After acknowledging that he has indeed ventured into other fields such as demography and politics, he then proclaims that

“If we are to deal adequately with processes of economic growth, processes of long-term change in which the very technological, demographic, and social frameworks are also changing—and in ways that decidedly affect the operation of economic forces proper—it is inevitable that we venture into fields beyond those recognized in recent decades as the province of economics proper…Effective work in this field necessarily calls for a shift from market economics to political and social economy.” (pg. 28)

And even more extraordinary remark, thoroughly ignored by most mainstream economists who keep pushing the inverted-U curve as a “law” of capitalist development.

A Peek at the Data

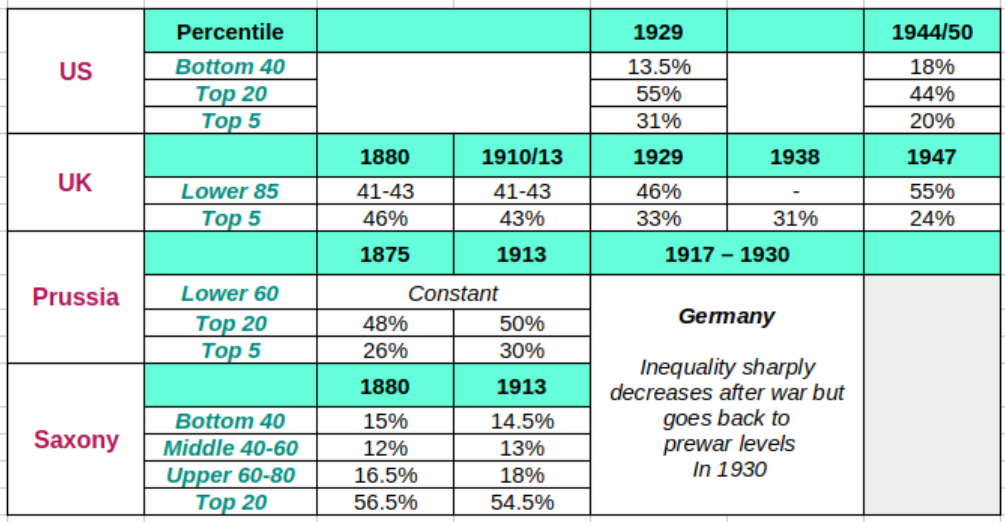

Despite Kuznets’ many warnings about the meagreness of the data, it is still surprising to find that fewer than 30 data points are supplied in section 2 to validate his hypothesis in advanced capitalist countries and regions. The table below summarizes these numbers.

Comparing data across countries is a bit tricky, as both observation years and income percentiles vary widely. Moreover, periodicity also changes across them. In the U.S., we have a range of 21 years, while the UK data covers 67 years. Prussia/Saxony are close to the U.S. range with 33, but cover very different years. That is important for determining what we mean by “long-term income inequality.”

The data show that inequality in both the U.S. and the UK is declining, albeit faster in the former. Note that the U.S. data for 1950 is the average Kuznets computed from previous years starting in 1944. From the U.S. data, we can calculate the middle 40-80 percentile to then create the lower 80 percentile. That number is 45% income share for 1939 and 56% for 1950. That is strikingly similar to the UK’s lower 85th percentile for comparative years. In other words, income inequality declines much faster in the U.S. and reaches levels similar to those of the UK, which took more than three times as long to get there. The case of Germany and its regions is clearly unique. Income inequality is fairly stable until 1913. It then decreases after the war but rises again after the 1929 economic crash. Therefore, we cannot say that income inequality decreased over time.

But even if it were decreasing slightly, the data would only show the declining part of the process for all three countries. In other words, the initial expected period of increased inequality as income begins to grow is missing. That is partly why the author decided to include data from developing countries still at the early stages of capitalist development. While he finds some evidence of this, he then suggests that in such countries, with comparatively low income, reducing long-term inequality might be challenging and may never occur. In that case, the Kuznets curve is not universally applicable.

Moreover, since we are only seeing the downward trend of inequality, we have to conclude that the inverted-U-shaped hypothesis holds over very long periods of time, between 42 and 134 years, as the case of the UK shows! Kuznets waves thus do not explain them. Kondratiev’s long waves have a better chance indeed.

That said, Kuznets draws the following carefully worded conclusion from this data:

“The general conclusion suggested is that the relative distribution of income, as measured by annual income incidence in rather broad classes, has been moving toward equality—with these trends particularly noticeable since the 1920’s but beginning perhaps in the period before the first world war.” (pg. 4).

He then adds three qualifications, two of which are relevant for our purposes. First, pre-tax income data excluding government transfers were used. Consequently, income shares for the lowest percentiles are underestimated as progressive taxation and increased government assistance prevailed at the time. That entails a faster decline in income inequality. However, as Piketty/Saez have shown, Kuznets did not include capital gains for the upper percentiles, thus underestimating top income shares.

The second qualification is even more relevant. The author argues that, over that period, per capita income has been increasing (except during war years). Assuming that such increases have the same rate across income percentiles, a reduction in inequality means that per-person income for lower-income groups is growing faster than that of higher-income groups.

Finally, nowhere in the paper do we find any reference to an “inverted-U-shaped curve” describing the interaction between inequality and economic growth. The closest we get comes from the following text:

“One might thus assume a long swing in the inequality characterizing the secular income structure: widening in the early phases of economic growth when the transition from the pre-industrial to the industrial civilization was most rapid; becoming stabilized for a while; and then narrowing in the later phases. This long secular swing would be most pronounced for older countries where the dislocation effects of the earlier phases of modern economic growth were most conspicuous. Still, it might be found also in the “younger” countries like the United States, if the period preceding marked industrialization could be compared with the early phases of industrialization, and if the latter could be compared with the subsequent phases of greater maturity.” (pg. 18)

Note the addition of a “younger” country, such as the U.S., but the exclusion of all developing countries, young and old. Note also the clearly spelled qualifiers for adding a younger country, which immediately eliminate most (though not all) developing nations. Kuznets is here hinting that his “long swing in … inequality” does not have a universal scope.

So where did the idea of a Kuznets “law” and the related “inverted-U-shaped curve” come from?

Raul